Businesses have worked so hard to learn about the COVID-19 relief programs available in the United States that some may be overlooking benefits available to them in other countries. Canada has enacted several programs that may apply to U.S. businesses — one of the most important for those with workers employed there is the Canada Emergency Wage Subsidy (CEWS). This program generally reimburses employers for 75% of employees’ wages if they’re employed during three qualifying periods between March 15 and June 6.

(The legislation also includes a provision giving the government the ability to extend the subsidy through Sept. 30, 2020.)

How CEWS works

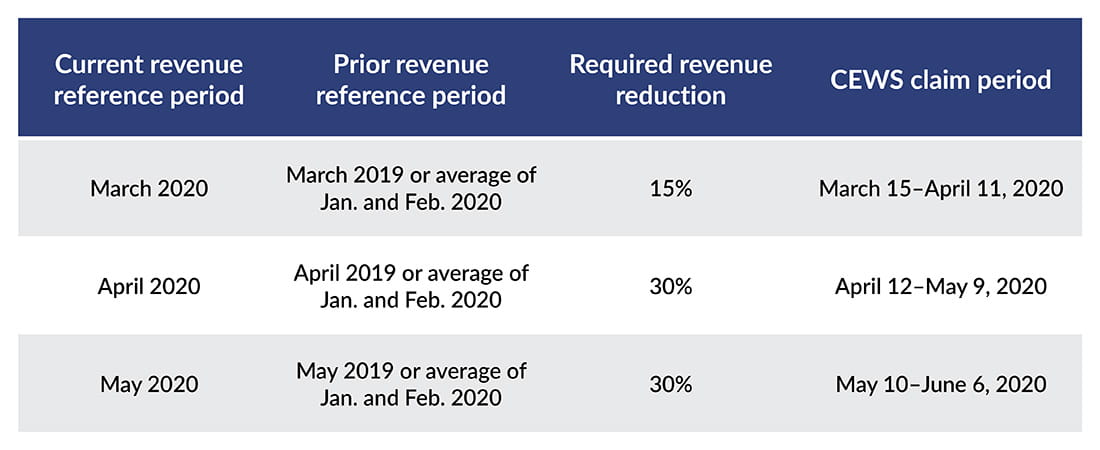

To qualify for the subsidy, you or your Canadian subsidiary must employ workers in Canada and you must suffer a “qualifying revenue reduction” in any of the three current reference periods (March, April, or May 2020) spelled out in the law relative to the prior revenue reference period.

If an employer’s qualifying revenue fell by 15% or more in March 2020 when compared to the qualifying revenue of either March 2019 or the average of January 2020 and February 2020 (the prior reference period), it would qualify to receive a subsidy for wages paid in respect of the period between March 15, 2020 and April 11, 2020 (the first CEWS claim period). Note that when making its first CEWS claim for the March 2020 current reference period, an employer must decide if it wants to use the average of January and February 2020 revenue or March 2019 revenue as its prior reference period. If the employer chooses to use March 2019 revenue as its prior reference period, it won’t have the option of using the average of January and February 2020 revenue as the prior reference period when making future claims.

While the subsidy is based on 75% of wages paid to each employee during a claim period, a higher subsidy percentage may result if an employee’s pay for a week during the claim period is less than their average pay from Jan. 1, 2020 to March 15, 2020 (pre-crisis wages). There is an expectation that employers who can, continue to pay wages at pre-crisis levels, but there is no requirement to that effect, so in some instances, an employer could get a 100% subsidy of wages paid.

Employers must apply separately for each claim period, although the deadline for submission isn’t until Sept. 30, 2020. A business doesn’t need to prove that the revenue decline is related to COVID-19.

Important considerations when looking at CEWS

The program provides considerable flexibility to employers in the application process, but many of those choices are locked in after the initial filing. As a result, businesses that can afford the cash flow repercussions may benefit from applying later in the process in order to make sure that they elect the options most favorable to them over the life of the program. Some of the choices available to employers that once made are locked in include:

- Calculating qualifying revenue on the cash or accrual basis.

- Comparing the current reference period qualifying revenue to qualifying revenue in the same month in 2019 or the average revenue in January and February of 2020.

- Calculating each employer’s revenue on a standalone basis or calculating on a consolidated basis if all of the revenue of the consolidated group is earned in Canada.

Unlike some of the U.S. relief programs, CEWS isn’t subject to a government budget limitation, so it will remain funded through the September 30 application deadline.

An employer can’t count an employee as eligible if that person wasn’t paid for a period of 14 days during a claim period, but the law does allow the employer to retroactively rehire that person, and the employee would count toward the subsidy as long as the retroactive pay and status meet the eligibility criteria for the claim period.

Of particular interest to U.S. businesses with subsidiaries in Canada is a provision that allows for an even broader calculation of qualifying revenue in order to qualify. If a Canadian employer derives more than 90% of its revenue from non-arm’s-length entities, special rules are available to calculate eligible revenue based on the non-arm’s-length entity’s revenue decline even if this revenue wasn’t earned in Canada and even if the non-arm’s-length entity isn’t a resident in Canada. Therefore, even if the Canadian employer’s revenue did not decline, CEWS may be available based on worldwide revenue in this instance.

Another significant difference between CEWS and many global COVID-19 relief programs is that there isn’t a requirement that the subsidy amounts be paid as additional wages or that the funds even remain in Canada. Since this is set up as a reimbursement for wages already paid, the government doesn’t track what the business does once it’s qualified for the funds. However, the government has indicated that it may publish the names of all employers who apply for the CEWS.

Finally, the CEWS is part of taxable income in Canada. All foreign programs should be evaluated to determine the impact on taxable income from a U.S. tax standpoint.

Canadian insights on CEWS

While CEWS is one of the most significant Canadian COVID-19 relief programs, it’s not the only one that may apply to your business. Canada is offering additional help in the form of commercial rent assistance, work-sharing programs, emergency loans, and tax payment deferrals. To understand how all of these programs work together, and to consider the many decisions that need to be made when applying for CEWS benefits, it’s important to discuss the options before filing for CEWS relief with the Canada Revenue Agency. In this case, your consultation should include a professional who’s familiar with Canadian rules.

For more information on how the Canadian CEWS program might help your business, please reach out to Linda Cook, Dana Hullinger, Ryan Luvisotto, or Carla Smaston.

This article was co-authored by Linda Cook and Ryan Luvisotto of Roth Mosey & Partners. Roth Mosey & Partners is a member of the Plante Moran Alliance, a group of independent accounting and professional service firms dedicated to helping member firms better serve their clients through group synergies.